Yes bank - say to inclusive and social banking and inclusive business model

- Monitoring, Evaluation and Learning

- by CSR Asia

- 26 Oct, 2015

Despite of the efforts made by banks in India to reach out to rural areas in recent years, India remains a highly unbanked country, with more than half of the population financially excluded. In 2004, Mr. Rana Kapoor left his job at a multinational bank and started YES BANK with a vision of driving inclusiveness and sustainability across India, and to serve the 600 million unbanked people.

YES BANK has an Inclusion and Social Banking (ISB) division that specialises in engaging the unbanked and under-banked populations in India. It uses sophisticated financial tools and adopts advanced technologies that are traditionally available only to big businesses, to develop offerings for the marginalised poor.

Approach

Launched in September 2011, YES Livelihood Enhancement Action Programme (YES LEAP) was one of the pioneer programmes that paved the way for many of the other financial inclusion products and services developed by the ISB division. YES LEAP provides comprehensive financial services, including credit, savings and micro-insurance, to women Self Help Groups (SHG). These groups are typically comprised of 10-20 women from local villages that make small regular contributions to a common fund. As the fund grows, money can be lent back to group members to meet their needs.

As indicated in the diagram, YES LEAP adopted a pioneer Business Correspondents (BCs) model. The BCs, which include NGOs, Self Help Promoting Institutions (SHPI) and SMEs that had already established long-term and credible connections with the SHGs, serve as an important nodal point for the facilitation of YES BANK’s financial inclusion services. The BCs typically provide financial inclusion education to the SHGs and help to introduce YES BANK’s products and services to the SHGs. After getting SHGs on board with the YES LEAP programme, the BCs are also involved in providing training to the SHGs and facilitate document collection and distribution. As a return for the BCs’ facilitation, YES BANK pays a commission fee, which is around 40-50% of the interest rate that the bank receives from the SHGs.

What also differentiates YES BANK from other existing lending channels is how it designs its products to adapt to the capability and demand of the women SHGs. Usually the most convenient way to borrow money for people in remote rural villages is from informal lenders in the villages that extend loans at an interest rate as high as 100%. While micro-finance institutions which are becoming more prevalent in recent years offer a lower interest rate than usuries, it is still difficult for women in rural villages to access credit as individuals because collateral is often needed. YES LEAP closes this gap through providing an unsecured group loan to women SHGs, offering an interest rate comparable to or even lower than micro-finance institutions. The nature of SHGs also ensures that each woman involved in these groups can have access to the fund when in need.

Outcomes

After four years of development, the YES LEAP programme has reached over 1.3 million women customers across 5,000 villages and disbursed a total of US$ 500 million in loans. The loan repayment rate is close to 100%. As mentioned by Mr. Sushanta Tripathy, vice president of the ISB division at YES BANK, considering the multiplier effect, YES LEAP’s cumulative disbursement has influenced almost US$1.5 billion in the Indian economy. Moreover, YES LEAP has made immeasurable impact on the women involved, contributing to the social empowerment and financial security of women, as well as enabling women entrepreneurs to develop their own businesses.

YES BANK has 42 partner BCs, with over 700 branches across 19 states in the country. The partnership and connection with SHGs has also enhanced YES BANK’s regional expansion, enabling other financial inclusion products to reach the rural villages. For example, YES BANK developed YES Kisan Dairy Plus, which provides an instant, secure and traceable payment solution specifically for farmers in rural areas. The access to women SHGs was of great value in introducing the YES Kisan Dairy Plus solution to the farmers that are either part of the SHGs or the relatives of SHG members.

Key Success Factors

• Business Correspondent model It has always been a challenge for banks to get access to remote rural villages due to physical barriers. It is essential that YES BANK managed to find the right grassroots partners that understand the financial inclusion needs and can also effectively facilitate with distribution and training activities. The effective feedback loop at the grassroots level also helps YES BANK improve the affordability and accessibility of the products and services.

• Real-time monitoring technology Very few banks in India have pushed the technology agenda like YES BANK. As the network of BCs and customers expanded, YES BANK was faced with the challenge of monitoring and tracking the programme in a timely manner. To tackle this challenge, YES BANK tapped into a vast network of service providers and invested in a real-time internet based communication system. This enables effective communication between YES BANK and the BCs across the country and also enhances the bank’s risk control mechanism.

Lessons Learned and Future Plans

In four years, YES BANK has grown into the leading social and inclusive banking service provider in India with an extensive network of low-income customers. However, YES BANK continues its innovation efforts – not only in relation to technology, but also in understanding the ever changing demands of customers. According to Mr. Tripathy, YES BANK has set a target to double the amount of loan disbursement under YES LEAP every year over the next 3-5 years. “The more customers we have, the higher expectations we receive. As customers have more access to credit, their needs will also evolve. We cannot afford stopping where we are - we need more innovation to adapt to our customers’ demand.”

In December 2014, YES BANK announced that it raised a loan of US$200 million from the Asian Development Bank (ADB) to take forward its objective of financial inclusion in India. The bank also received US$1 million in aid to improve its real-time monitoring platform. This is expected to strengthen YES BANK’s position in expanding its financial inclusion services across India.

The India Responsible Business Forum (IRBF) Index 2015 is an initiative by Oxfam India in partnership with Corporate Responsibility Watch, Praxis and Partners in Change, non-profits which look at corporate accountability and business responsibility.

References

1.ADB (2014), “ADB $200 million loan to YES BANK helps rural women, small-holder farmers”. http://www.adb.org/news/adb-200-million-loan-yes-bank-helps-rural-women-small-holder-farmers (accessed September 24, 2015)

2.Asli Demirguc-Kunt, Leora Klapper, Dorothe Singer and Peter Van Oudheusden (2015), “The Global Findex Database 2014 : measuring financial inclusion around the world,” World Bank Group. http://www-wds.worldbank.org/external/default/WDSContentServer/WDSP/IB/2015/04/15/090224b082dca3aa/1_0/Rendered/PDF/The0Global0Fin0ion0around0the0world.pdf (accessed September 30, 2015)

3.First Post (2013), “YES Bank’s Kapoor explains why getting a bank license is a long haul for aspirants”. http://www.firstpost.com/business/getting-a-bank-licence-a-long-haul-for-aspirants-says-yes-bank-844165.html (accessed September 30, 2015)

4.Interview with Mr. Sushanta Tripathy, vice executive president of ISB Division at YES BANK on October 15, 2015.

5.Mohd Mustaquim (2015), “Mobile technology shaping agriculture,” Rural Marketing. http://www.ruralmarketing.in/industry/agriculture/mobile-technology-shaping-agriculture (accessed September 30, 2015)

6.Namita Vikas (2015), “Innovation in Sustainable Finance,” European Organisation for Sustainable Development (EOSD). http://www.eosd.org/en/gsfc2015/day1/Namita_Vikas_Yes_Bank.pdf (accessed September 30, 2015)

7.Navi Radjou, Jaideep Prabhu and Simone Ahuja (2010), “In India, Looking for a Sustainable Capitalism,” Havard Business Review. https://hbr.org/2010/05/in-india-looking-for-a-sustain (accessed September 24, 2015)

8.Raghav Narsalay and Ryan T. Coffey (2013), “Inclusive business initiatives: Scaling innovation for an emerging middle class,” Accenture. https://www.accenture.com/t20150522T061605__w__/us-en/_acnmedia/Accenture/Conversion-Assets/Outlook/Documents/1/Accenture-Outlook-Inclusive-Business-Initiatives-Scaling-Innovation-For-An-Emerging-Middle-Class.pdf#zoom=50 (accessed September 24, 2015)

9.World Forum Lille (2010), “Yes Bank: When financial solutions help solve social problems,” BipiZ. http://www.bipiz.org/en/advanced-search/yes-bank-when-financial-solutions-help-solve-social-problems.html (accessed September 29, 2015)

10.YES BANK website (2014), “YES BANK raises USD 200 mn unsecured loan from Asian Development Bank”. https://www.yesbank.in/media-centre/press-releases/fy-2014-15/yes-bank-raises-usd-200-mn-unsecured-loan-from-asian-development-bank.html (accessed September 24, 2015)

11.YES BANK (2014), “The YES Bank story: Building the finest quality bank of the world in India”. https://www.yesbank.in/images/all_pdf/YBLStoryNew_17Nov2014.pdf (accessed September 24, 2015)

Monitoring, Evaluation and Learning

Monitoring, Evaluation and Learning at Oxfam India plays essential function of gathering evidence to measure the degree to which our interventions bring sustainable changes in people's lives

Read MoreRecent Blogs

Making Sanitation & Hygiene Facilities Accessible—Delhi Flood Response

Aug 4, 2023 | Savvy

Psychosocial Counselling for Balasore Train Tragedy Survivors

Jul 6, 2023 | Savvy

The Oxfam India Legacy Will Live On

May 30, 2023 | Savvy

Inequality In Parliament

Mar 31, 2023 | Savvy

International Women's Day Round Up

Mar 30, 2023 | Savvy

Why Women in India Earn Less And Get Fewer Jobs—Discrimination

Mar 2, 2023 | Savvy

The Inequality Issue

Jan 17, 2023 | Savvy

Oxfam India in 2022: 10 People 10 Stories

Mar 9, 2023 | Savvy

Boosting the Rural Economy | Parab Festival

Dec 23, 2022 | Savvy

Striving for Financial Inclusion: Need Women-Friendly Ecosystem

Dec 2, 2022 | Savvy

Primary Prevention of Violence Against Women and Girls And the Role of Civil Society Organisations

Nov 28, 2022 |

Bottom Up Approach: Strengthening School Management Committees For Better Schools

Nov 22, 2022 | Savvy

Disconnecting 1098 Is A Bad Idea

Nov 14, 2022 | Savvy

11 Facts About Education In India That You Need To Know

Oct 31, 2022 | mahika@oxfamindia.org

Assam Floods | Our Response Updates

Oct 3, 2022 | Savvy

India Discrimination Report | 8 Things You Need To Know

Sep 15, 2022 | Savvy

For The Youth To Rise Against Inequality, We Must Work With Them

Aug 12, 2022 | Savvy

The Consequences of School Closures on Adivasi Children

Aug 9, 2022 | Savvy

Celebration of Iconic Days In Mohalla Classes

Jun 29, 2022 | Savvy

Financial Literacy Awareness Continues

Jun 29, 2022 | Savvy

I Want To Join The Army

May 30, 2022 | Savvy

Financial Literacy Camps For Women Farmers

May 30, 2022 | Savvy

Education Opens The Doors Of Freedom, Yet Again

May 5, 2022 | Savvy

Bitter Sugar: Cane Cutters Charter of Demands

May 26, 2022 | Savvy

International Women's Day | The Week That Was

Mar 21, 2022 | Savvy

Building A Responsible Sugar Supply Chain

Feb 20, 2022 | Savvy

Empowerment Not Age: Examining The Complexities Of Child, Early And Forced Marriages

Feb 16, 2022 | Savvy

Dominance by Billionaires Leads India’s Highway to Record Levels of Inequality

Jan 25, 2022 | Savvy

Why We Need To Stand Up For The Cane Cutters

Jan 13, 2022 | Savvy

फ़ातिमा शेख़: देश की पहली मुस्लिम शिक्षिका को नमन

Jan 9, 2022 | Savvy

2021: Your Journey With Oxfam India

Dec 31, 2021 | Savvy

Policing Adolescent Sexuality And Health Consequences

Jan 17, 2022 | Savvy

16 Days of Activism

Dec 17, 2021 | admin

Women's Land Rights Are Human Rights

Dec 16, 2021 | Savvy

A Child-Friendly Environment Is Essential To Children's Rights

Dec 14, 2021 | Savvy

Urban Food Hive Project: Nourish The Cities

Feb 28, 2022 | Savvy

महिलाओं को मिले बराबरी का हक तो बदल सकती है खेती-किसानी की सूरत

Oct 15, 2021 | Savvy

Only Together… Can We Save Our Rivers!

Oct 12, 2021 | Savvy

Chhattisgarh Roundtable: Implementation of PWDVA

Oct 10, 2021 | Savvy

Multi-Stakeholder Consultation on Fisheries Management

Oct 10, 2021 | Savvy

What Sugarcane Farmers Want

Oct 8, 2021 | Savvy

How Unequal is Inequality?

Oct 6, 2021 | Savvy

Bring Teachers To School: UP’s Unfilled Vacancies and Its Impact

Oct 4, 2021 | Savvy

The Case of Low Conviction in Crimes Against Dalits and Adivasis

Sep 29, 2021 | Savvy

शिक्षा से वंचित बच्चों को विद्यालय में लाने की मुहीम

Oct 10, 2021 | Savvy

Initiating Work With Cane Cutters in Maharashtra

Sep 16, 2021 | Savvy

शिक्षक दिवस पर सावित्री बाई फुले को श्रद्धांजलि

Sep 5, 2021 | Savvy

Questions On Healthcare, Education And Inequality Raised In Parliament

Sep 1, 2021 | Savvy

ट्रोसा परियोजना के क्रियान्वयन से जागरूक हुआ ग्रामीण समुदाय

Sep 15, 2021 | Savvy

Oxfam India Pushes for Implementation of Patients’ Rights Charter

Aug 7, 2021 | Savvy

Cyclones, Flood, and COVID-19 Upends Lives in Odisha’s Soro Block

Jul 23, 2021 | Savvy

SDG Index: A Long Way To Go

Jul 7, 2021 | Savvy

Our Women Water Champions

Jun 4, 2021 | Savvy

COVID-19 in Assam’s Tea Gardens

May 17, 2021 | Savvy

Informal Sector Workers In A Policy Blind Spot

Jun 7, 2021 | Savvy

Positive Gender Social Norms For A Better Society

Apr 15, 2021 | Savvy

From Conflict to Cooperation

Apr 9, 2021 | Savvy

Oxfam India journey to end discrimination – glimpses from 2020

Apr 1, 2021 | Anisha

Oxfam India's International Women’s Day Celebrations

Mar 14, 2021 | Savvy

Forest Rights Recognised In Jharkhand for the First Time in Two Years

Mar 12, 2021 | Savvy

छत्तीसगढ़ बजट 2021: वनाधिकार के नजरिये से

Mar 2, 2021 | Savvy

Transforming Lives Of Tribal Women With Energy Efficient Cook-Stoves

Feb 19, 2021 | Savvy

The Inequality Virus Released in States

Feb 14, 2021 | Savvy

Implementing Patients’ Rights Charter: Step towards Accessible Health

Jan 12, 2021 | Savvy

To Be or Not To Be: Minimum Age of Marriage for Girls

Jan 12, 2021 | Savvy

Addressing Early Marriages in India (Oxfam India-SAWM Webinar)

Dec 23, 2020 | Savvy

The Right Age for Marriage: Should the State Decide?

Dec 3, 2020 | Savvy

#EmpowermentNotAge

Jan 4, 2021 | radhika

#EmpowermentNotAge

Apr 1, 2021 | radhika

5 Reasons Changing The Minimum Age Of Marriage Is A Bad Move

Dec 23, 2020 | radhika

The Status of Implementation of PWDVA: Odisha Consultation

Sep 30, 2020 | Savvy

Right To Property: An Imperative For Freedom

Sep 30, 2020 | Savvy

A Salute to the Architects of Our Society

Sep 30, 2020 | Savvy

शारदा नदी बेसिन में सिंचाई की पद्धतियों पर एक अनुभव

Sep 30, 2020 | Savvy

Chhattisgarh Recognises CFR Rights – A First Since FRA’s inception

Aug 25, 2020 | Savvy

Legal Reforms to Increase Age of Motherhood — Will It Work?

Sep 30, 2020 | radhika

समानता के सिद्धान्त को आदिवासी सिखलाता है

Aug 9, 2020 | Savvy

The Need to Uphold RTE Act During a Pandemic

Aug 5, 2020 | Savvy

My Internship Experience at Oxfam India

Aug 21, 2020 | radhika

Comprehensive Regulatory Framework for Private Schools Needed

Aug 4, 2020 | Savvy

Measures to Increase Reporting of Domestic Violence, a Parallel Pandemic

Sep 30, 2020 | radhika

Locked-down: Domestic Violence Reporting in India during COVID-19

Sep 30, 2020 | radhika

Agriculture & COVID-19: Pro Women Farmer Policies Needed

Aug 1, 2020 | Savvy

The Loot of Private Healthcare

Jul 17, 2020 | Savvy

Protecting Children's Rights during Lockdown

Jul 15, 2020 | Savvy

The SWaCH Story | How waste pickers continued work during lockdown

Mar 5, 2021 | Savvy

Inclusive Economic Opportunities for Brahmaputra River Communities

Jun 30, 2020 | Savvy

How can India’s education system escape the vicious cycle of inequality and discrimination?

Jun 30, 2020 | radhika

Haq Se… We (He, She and Ze) are all Equal!

Jun 30, 2020 | Savvy

Living the Rainbow Dream

Jun 30, 2020 | Savvy

Tea Workers in a Tough Spot

Jun 30, 2020 |

Mental Health In COVID-19

Jun 30, 2020 | radhika

Milk for the Twins

Jun 24, 2020 |

The COVID-19 Impact on Waste Pickers in Delhi

Jun 24, 2020 |

Yes, It is That Time of the Month!

Jun 30, 2020 |

It is Raja Festival, Let’s Talk about Periods

Jun 15, 2021 |

पर्यावरण बचाना होगा

Jun 30, 2020 | Savvy

COVID-19 Is Covering For Nature, Are We?

Jun 30, 2020 | radhika

Cyclone Amphan’s Trail of Devastation

Jul 29, 2020 | Savvy

COVID-19 Pandemic: Oxfam India is Responding

May 31, 2020 | Savvy

Oxfam India Prepares Ahead of Cyclone Amphan Landfall

Jul 29, 2020 | Savvy

On Foot, On Truck and Finally, A Bus

May 31, 2020 | Savvy

Getting Home, Somehow

May 31, 2020 | Savvy

COVID Lockdown Makes Meeting Ends Difficult

May 31, 2020 | Savvy

A Bleak Future

May 28, 2020 | Savvy

A virus that exploits racism

May 31, 2020 | radhika

COVID-19 Reveals Deep Vulnerabilities in India’s Labour

May 31, 2020 |

COVID-19 CSR Appeal By Oxfam India

May 31, 2020 | radhika

Recognising land rights this International Day of Forests

May 31, 2020 | radhika

Covid Cooperation: United We Survive

May 31, 2020 | Animesh Prakash

Coronavirus and Inequality

May 31, 2020 | radhika

Government of Odisha releases Climate Budget 2020-2021

May 31, 2020 | radhika

Feminism through Movies at the Raipur film festival

Jun 3, 2020 | radhika

How Oxfam India Transformed Lives in 2019

Jun 3, 2020 | Anisha

The Story Behind Beyond Charity (Oxfam India's 10 Year Journey)

Jun 3, 2020 | radhika

Rapid Needs Assessment for Unprecedented Floods in Uttar Pradesh

Jun 3, 2020 | radhika

Access to energy for livelihood security

Dec 5, 2019 | radhika

Truth About Tea Campaign at Lucknow's Kabir Festival

Jun 3, 2020 | radhika

Reflections from UN Forum on Business and Human Rights 2019

Dec 18, 2019 | radhika

State Consultation Meeting on Forest Rights Act 2006

Dec 5, 2019 | radhika

Say yes to #EqualWaliDiwali

Dec 5, 2019 | radhika

Do a Good Deed and Save Tax

Oct 23, 2019 | Anisha

Youth spearhead the #CleanPatnaDrive in Bihar

Dec 5, 2019 | radhika

Celebrate Daan Utsav with Oxfam India

Oct 9, 2019 | radhika

Forest rights leading to livelihood security

Oct 9, 2019 | radhika

Love is always violence free

Dec 5, 2019 | radhika

Long wait, delayed returns

Dec 18, 2019 | radhika

Environmental cost of sugar

Sep 25, 2019 | radhika

Giving up not an option for women farmers

Dec 18, 2019 | radhika

Workers in sugarcane farms of Uttar Pradesh get a bitter deal

Sep 25, 2019 | radhika

5 takeaways from Study on Sustainability in Sugar Value Chains

Sep 25, 2019 | radhika

Code on Wages lacks clear policy outcome

Nov 21, 2019 | radhika

Caste, Class and Education

Sep 19, 2019 | radhika

Trailblazing on the Path to Education4All

Dec 5, 2019 | radhika

Background Note: State Convention on Proposed Amendments to Indian Forest Act 1927

Feb 20, 2020 | radhika

Recommendations on proposed amendments to the Indian Forest Act 1927

Dec 18, 2019 | radhika

Oxfam India’s Response to Natural Disasters

Dec 5, 2019 | Anisha

Celebrating Women Humanitarians | World Humanitarian Day 2019

Aug 19, 2019 | radhika

जारी है ऐतिहासिक अन्याय

Dec 18, 2019 | radhika

Life at Oxfam India

Dec 18, 2019 | radhika

Why should you make Humanitarian donations to an NGO?

Dec 5, 2019 | radhika

The scourge of manual scavenging

Dec 5, 2019 | radhika

Trailwalker- the ultimate walkathon for a social cause

Dec 18, 2019 | radhika

Making Communities Resilient in Flood-Prone Bihar

Dec 18, 2019 | Anisha

Obligations & choices- the unceasing dilemma

Dec 5, 2019 | radhika

Course on Business and Human Rights – 3rd Edition

Aug 1, 2019 | radhika

जंगल की कविताएं

Jul 31, 2019 | radhika

It is not your job | Unpaid care work in India

Dec 5, 2019 | radhika

Rural healthcare in India — a boon or bane?

Dec 18, 2019 | radhika

For the Gonds, Forest is Heaven on Earth

Dec 5, 2019 | radhika

The Case of Incomplete CFR Titles of Arjuni Village

Dec 5, 2019 | radhika

Oxfam India stands with flood-affected families in Assam

Dec 5, 2019 | Anisha

Undo Historical Injustice to Forest Dwellers, Once Again

Dec 5, 2019 | radhika

Empowering women, one step at a time

Dec 18, 2019 | radhika

Encephalitis is ending our future- our children

Dec 5, 2019 | radhika

#YesDemocracy | Creating fearless spaces for all

Jun 27, 2019 | radhika

Oxfam India collaborates with Josh Talks

Jun 19, 2019 | radhika

Oxfam India pushes for proper implementation of FRA in Chhattisgarh

Dec 18, 2019 | Anisha

Oxfam India’s Community Leader Wins Woman Exemplar Award 2019

Sep 27, 2019 | Anisha

Rebuilding cyclone-affected lives in Odisha

Jun 19, 2019 | Anisha

Marginalised communities in UP fight for their right to healthcare

Dec 18, 2019 | Anisha

Women’s Health on the Backburner in Bihar’s Poll

May 27, 2019 | sanya

Vote for a New India! #YesDemocracy

May 24, 2019 | Anisha

Oxfam India thinks out-of-the-box to restore wells in Kerala

Jul 23, 2020 | ursila

Oxfam’s Learning Lab on Private Sector Engagement

Sep 9, 2019 | ursila

Help Meena break the endless cycle of poverty through education

Sep 9, 2019 | Anisha

Rampant discrimination at Public Health Facilities- Aarti's story

Sep 9, 2019 | ursila

“The IT girl” – Breaking the stereotype of women in tech

May 13, 2019 | ursila

How Oxfam India touched lives in 2018

Sep 30, 2019 | ursila

Five Charities Working For Women

Sep 19, 2022 | ursila

Oxfam India's latest workshop on 'Threat to media, Fake News & #MeToo'

Sep 10, 2019 | ursila

Everything you must know about Oxfam India's fight against inequality

Oct 24, 2019 | ursila

What does Delhi have to say about India's Inequality Problem?

Oct 7, 2019 | ursila

What is Inequality?

Oct 24, 2019 | ursila

Jalaun's Manual Scavengers- Fighting for Right to Life with Dignity

Feb 20, 2020 | ursila

World Wetlands Day- Is India committed towards wetland conservation?

Nov 11, 2019 | ursila

Collective Action integral to Transboundary Risk Governance

Oct 30, 2019 | ursila

Childcare in India today

Jun 3, 2020 | ursila

Oxfam India takes the fight against inequality to the streets

Nov 18, 2019 | ursila

Five moments from 2018 that emboldened the fight for gender justice

Sep 27, 2019 | ursila

Seven frequently asked questions about Oxfam’s Inequality report

Oct 7, 2019 | ursila

Pratima, a casualty of India's growing inequality

May 31, 2020 | ursila

10 powerful quotes to help you understand the global inequality crisis

Oct 24, 2019 | ursila

Inequality through my lens

Oct 24, 2019 | ursila

Achieving water rights by smashing patriarchy

Oct 24, 2019 | ursila

Chennai's resettlement colony shows a grim picture of Inequality

Oct 24, 2019 | ursila

Art Meets Activism with the Illustrate For Impact Fellowship - Register Now

Apr 5, 2019 | ursila

Oxfam India organized two state level consultations under education program

Nov 18, 2019 | Anisha

Secret Superstar: On fighting domestic violence and finding autonomy

Sep 27, 2019 | ursila

Failed Education Priorities of the Bihar Government

Feb 20, 2020 | ursila

Structural injustice in Sugar Cane Agriculture

Sep 9, 2019 | ursila

Addressing malnutrition during a humanitarian crisis

Oct 7, 2019 | ursila

My first experience of handling a natural disaster

Oct 7, 2019 | ursila

15 Healthcare schemes in India that you must know about

Sep 23, 2019 | ursila

Oxfam India marks "16 Days of Activism"

Oct 24, 2019 | Anisha

This unique search engine aims to tackle energy poverty in rural India

Sep 10, 2019 | ursila

10 things you need to know about the RTE Act #HaqBantaHai

Sep 27, 2019 | admin

Two women human rights defenders on the power of mobilisation

Oct 24, 2019 | ursila

Oxfam India Celebrates Child Rights Week

Oct 31, 2019 | oxfamadmin

10 women-led protests that shook the world in 2018

Oct 7, 2019 | ursila

Achieving the SDGs is impossible without empowering Indian women

Apr 5, 2019 | ursila

Social Norms Simplified

Feb 20, 2020 | admin

Child Labour & Child Rights in India: Myth or Reality

Sep 9, 2019 | ursila

Be a ChangeMaker with Oxfam's latest free course on Campaigning, Advocacy and Community Mobilisation

Apr 5, 2019 | admin

Is India committed to reducing inequality? This report finds out more

Sep 9, 2019 | ursila

Oxfam India introduces a course on Gender & Media

Oct 7, 2019 | admin

Section 377 Scrapped: Supreme Court's Verdict Creates History

Oct 7, 2019 | admin

Why I joined the fight for Gender Equality

Oct 24, 2019 | admin

Who is Reaping the Benefits of India’s High Economic Growth?

Oct 24, 2019 | admin

Oxfam India's stand on allegations of sexual harassment against filmmaker of Balekempa

Apr 5, 2019 | admin

Oxfam India's CEO, Amitabh Behar on India's commitment to reduce inequality

Oct 24, 2019 | admin

Move over 'Sons of the soil': Why you need to know the female farmers that are revolutionizing agriculture in India

Oct 7, 2019 | admin

Oxfam India stands in solidarity with #MeToo movement

Oct 24, 2019 | admin

Road to rebuilding “God’s own country” | Aftermath of Kerala Floods

Apr 5, 2019 | admin

Mystery of Out-of-School-Children in the Indian Education System

Sep 27, 2019 | admin

A school with no roof

Oct 24, 2019 | ursila

Oxfam India helping mothers deliver healthy babies

Apr 5, 2019 | Anisha

How Oxfam India is helping crack gender stereotypes in the Indian Film Industry

Oct 24, 2019 | Anisha

Rhymes and plays unite children on Global Handwashing Day

Sep 27, 2019 | Anisha

Why India's girl child deserves a chance at education

Sep 12, 2022 | admin

Oxfam India reaches to over 15,000 people in Kerala

Apr 5, 2019 | Anisha

Oxfam India responds to sexual misconduct by Oxfam GB staff during Haiti Earthquake response in 2010

Oct 7, 2019 | ursila

Oxfam Stands with Kerala

Oct 1, 2019 | Anisha

Oxfam helped over 25,000 people within three months

Oct 30, 2019 | Anisha

Oxfam India engages with youth on ‘Inequality in Education’

Oct 7, 2019 | Anisha

Four reasons why the Forest Rights Act fails to empower forest-dwelling communities

Oct 7, 2019 | ursila

Stories from the ground: Oxfam India’s response to floods 2018

Oct 24, 2019 | Anisha

North East Floods 2018: Oxfam is responding

Apr 5, 2019 | Anisha

Oxfam India’s champion: Megha

Sep 10, 2019 | Anisha

Stories of Change: Scripting Her Own Fate

Oct 7, 2019 | ursila

In pursuit of justice…

Oct 24, 2019 | ursila

Can we afford to overlook Assam Floods?

Oct 7, 2019 | ursila

Everything you need to know about Oxfam India’s response to Assam Floods 2017

Oct 24, 2019 | ursila

How does Oxfam respond during humanitarian disasters like floods?

Oct 24, 2019 | ursila

Oxfam India responds to North East floods 2018

Oct 30, 2019 |

Stories of Change: Strike back the silence

Oct 7, 2019 | ursila

Oxfam’s campaign on Access to Affordable Essential Medicines

Oct 7, 2019 | Anisha

Oxfam’s training programs saving lives

Oct 7, 2019 | Anisha

Chiligi’s fight for education

Oct 1, 2019 | Anisha

Where there is a Will, there is a Way

Oct 7, 2019 | Anisha

Stories of Change: Fighting against all odds

Sep 27, 2019 | ursila

Stories of Change: Breaking Boundaries at Home

Oct 24, 2019 | ursila

Stories of Change: Rise. Resist. Rebel

Oct 1, 2019 | ursila

Stories of Change: Celebrating our feminist heroes

Nov 14, 2019 | ursila

3 Innovations in Disaster Risk Reduction in India you should know about

Oct 24, 2019 | ursila

Oxfam India Disaster Risk Reduction Program Continues

Oct 1, 2019 | Anisha

Oxfam India Builds Water Solution in Disaster Prone Areas

Oct 24, 2019 | Anisha

A Second Chance at Life

Oct 7, 2019 | Anisha

5 books that will change the way you see the world around you

Oct 7, 2019 | ursila

Meet these 3 Warriors who are Fighting Inequality through Education

Apr 5, 2019 | ursila

Meet these 3 Warriors who are Fighting Inequality through Education

Nov 18, 2019 | Anisha

Oxfam India’s innovation building resilient communities.

Sep 9, 2019 | Anisha

Is ineffective healthcare system affecting lives?

Sep 10, 2019 | Anisha

Breaking the shackles of domestic violence

Nov 21, 2019 | Anisha

Listening To The Unheard Voices Of India

Oct 7, 2019 | Anisha

Empower Women, Empower Nation- Oxfam India on International Women’s day

Sep 10, 2019 | Anisha

Yet another International Women’s Day, Yet another Struggle

Sep 27, 2019 | ursila

15 shocking facts about inequality in India

Oct 24, 2019 | ursila

NGOs Strengthening the Education System in India

Sep 20, 2022 | Anisha

Oxfam India’s Humanitarian Champions

Nov 11, 2019 | Anisha

Changing Social Norms Through Education

Oct 7, 2019 | Anisha

The Power of Courage

Oct 24, 2019 | Anisha

Healthcare Awareness Saves Lives

Oct 1, 2019 | Anisha

A World Free From Violence Against Women

Sep 10, 2019 | Anisha

BRIDGING THE GAP

Oct 24, 2019 | Anisha

DISABLING THE DISABILITY

Oct 30, 2019 | Anisha

Children are paying the price of Tax Robbery. Help Stop This. Give A Missed Call on 70977 70977

Oct 1, 2019 | ursila

India’s children are paying the price of Tax Robbery

Oct 24, 2019 | ursila

Reel & Real: Blurred Lines between Cinema and Reality- Notes from Women In Films brunch at Jio MAMI Film Festival

Oct 30, 2019 | ursila

Oxfam Gave Relief to Over 82,000 Lives

Oct 30, 2019 | Anisha

Picture Abhi Baqi Hai, Behena

Oct 1, 2019 | ursila

Assam Drowns Again

Sep 27, 2019 | Anisha

A Long Road Home

Oct 7, 2019 | Anisha

Oxfam India’s letter to President of India requesting affirmative action on passing Women’s Reservation Bill in Parliament.

Sep 10, 2019 | oxfamadmin

Women Representation in Political Decision Making: A Catalyst to achieving Gender Equality

Oct 24, 2019 | ursila

Will Fear of ‘Failing’ Make India Literate?

Sep 27, 2019 | ursila

WATER IS LIFE

Nov 18, 2019 | Anisha

Building bridges: The journey of a teacher par excellence

Oct 7, 2019 | ursila

Examining humanitarian aid through the gender lens

Oct 24, 2019 | ursila

The pathways to gender equality are far from straight

Oct 7, 2019 | ursila

The changing world of humanitarian work

Sep 10, 2019 | ursila

Can India be a Leader in Disaster Risk Reduction Measures in Asia?

Oct 7, 2019 | ursila

A struggle for survival: Assam Floods

Nov 11, 2019 | Anisha

Lessons to be learnt from the Gorakhpur tragedy

Oct 24, 2019 | ursila

Is Section 498A anti women?

Nov 11, 2019 | ursila

The Irresistible & Oppressive Gaze: A Survey Report by Oxfam India

Oct 24, 2019 | oxfamadmin

North East Floods: How you can help those affected?

Oct 1, 2019 | Ravi

Oxfam is responding in Assam Floods 2017

Oct 1, 2019 | Ravi

Lipstick Under My Burkha Official Trailer - Winner of Oxfam's Best Film on Gender Equality Award

Sep 27, 2019 | Ravi

Sourcing Life

Oct 7, 2019 | Anisha

MEETING TOILET TARGETS

Oct 7, 2019 | oxfamadmin

Disaster Changed Her Life

Oct 24, 2019 | Anisha

#HaqBantaHai Campaign on Access to Free Medicine: Bihar

Sep 10, 2019 | Anisha

Be The New Norm

Oct 7, 2019 | Ravi

Oxfam India’s Recommendations for National Policy for Women

Sep 27, 2019 | Ravi

The Greatest Earning: EDUCATION

Dec 5, 2019 | Anisha

Women Farmers or Labourers?

Oct 24, 2019 | Avantika

Farewell Dirty Water

Jan 9, 2020 | Avantika

Clean Water Can Save Lives

Oct 24, 2019 | Avantika

Making men an ally on women's rights

Oct 24, 2019 | Avantika

'Initially the men opposed. They thought we women were being disruptive.'

Oct 1, 2019 | Avantika

Tax havens resist reforms one year on from Panama Papers exposé

Oct 1, 2019 | Avantika

इख़्तियार

Oct 24, 2019 | Avantika

Lessons from the Grassroots

Sep 10, 2019 | Avantika

This is What Child Marriage Looks Like

Nov 18, 2019 | Avantika

Oxfam India Held Youth Festivals In Lucknow And Raipur

Sep 9, 2019 | Avantika

Oxfam at the North-East Disaster Risk Reduction Conclave 2017

Sep 9, 2019 | Avantika

Finding Solutions to Early and Forced Marriage

Sep 27, 2019 | Avantika

Silence Has No Honour

Sep 27, 2019 | Avantika

Solidarity Is Our Weapon- The International Women’s Strike

Oct 24, 2019 | Avantika

4 reasons why Oxfam supports the International Women’s Strike on the 8th March

Oct 24, 2019 | Avantika

Union Budget 2017-18: Neglected Social Sector

Sep 10, 2019 | Avantika

Putting Data at the Heart of Business Responsibility

May 13, 2019 | Avantika

Mainstreaming DRR in Local Development Plans to Reduce Aid Dependency

Oct 1, 2019 | Avantika

Union Budget 2017-18: A Look at the Health Sector

Apr 5, 2019 | Avantika

खेल - जेण्डर आधारित असमानताओं को उजागर करने को एक सषक्त माध्यम

Apr 5, 2019 | oxfamadmin

Why Brazil should not take a U-turn on its health system

Oct 7, 2019 | Avantika

Your questions answered: Oxfam’s Inequality report

Oct 1, 2019 | Avantika

Unpacking the Risks of Doing Business in India

Nov 14, 2019 | Avantika

We Never Learn

Sep 27, 2019 | Ravi

Promote men’s involvement for changing social norms

Oct 24, 2019 | Avantika

Ten years of the Forest Rights Act: Opportunity lost?

Oct 1, 2019 | oxfamadmin

Meet the Bravehearts Standing Up Against Domestic Violence

May 27, 2020 | oxfamadmin

Addressing Violence Against Women and Girls the SAARC Way: Combat Human Trafficking

Sep 10, 2019 | oxfamadmin

Oxfam India’s journey from programme to campaign

Oct 24, 2019 | oxfamadmin

सामाजिक मान्यताओं को चुनौती देता संगठन

Dec 5, 2019 | oxfamadmin

Changing The World – One Couple At A Time

Oct 24, 2019 | oxfamadmin

A Lesson on Education from Uttar Pradesh

Oct 7, 2019 | oxfamadmin

Fair Sharing of Mining Revenue for the Tribals

Oct 24, 2019 | oxfamadmin

An Open Letter to Chhotu, Munna and Bachcha

Jun 12, 2020 | oxfamadmin

Educating the Educators

Sep 27, 2019 | oxfamadmin

10 Years of Domestic Violence Act: The Way Ahead

Oct 24, 2019 | oxfamadmin

Oxfam Best Film on Gender Equality Award Gets Grand Reception

Sep 27, 2019 | oxfamadmin

Wrestling Social Norms Out

Oct 3, 2019 | oxfamadmin

The Toilet Conundrum

Oct 24, 2019 | oxfamadmin

Inequality in India: what's the real story?

Sep 27, 2019 | oxfamadmin

Making surface water safe for drinking

Oct 1, 2019 | oxfamadmin

Quality Education- The unfinished agenda of RTE Act

Sep 27, 2019 | oxfamadmin

Tale of Two Women

Sep 27, 2019 | oxfamadmin

Prioritising the Health of our Children

Oct 24, 2019 | oxfamadmin

Violence in women’s own backyard

Sep 9, 2019 | oxfamadmin

We failed yet again

Sep 10, 2019 | oxfamadmin

Providing access to iron-free drinking water

Oct 7, 2019 | oxfamadmin

Her Series - Tale of Buguru Chitamma: How a cooperative transformed fisher women into leaders

Oct 24, 2019 | oxfamadmin

Why the CAF bill conflicts with the Forest Rights Act?

Oct 7, 2019 | oxfamadmin

Renew to Live Anew

Sep 9, 2019 | oxfamadmin

What do we want: Health as a ‘Right’ or just an ‘Assurance’

Nov 18, 2019 | oxfamadmin

Oxfam International signs historic deal to move to Nairobi, Kenya

Oct 24, 2019 | oxfamadmin

Why is passing the Women’s Reservation Bill urgent?

Sep 19, 2023 | oxfamadmin

BREXIT & What It Means for Humanitarian Aid

Oct 7, 2019 | oxfamadmin

Rahul Bose: Films should be gender sensitive

Oct 24, 2019 | oxfamadmin

Portrait of a Teacher: Successful introduction of multi-lingual education for Odisha’s tribal communities

Nov 6, 2019 | oxfamadmin

Tax dodging is a crime against developing countries

Sep 10, 2019 | oxfamadmin

Signs of social risks impacting Indian businesses

Oct 7, 2019 | oxfamadmin

Tikamgarh revisited, what’s happened to the amazing fishing communities I visited in 2006?

Jan 9, 2020 | oxfamadmin

Where school means freedom

Sep 10, 2019 | oxfamadmin

Yes, Prime Minister

Oct 30, 2019 | oxfamadmin

India’s National Budget 2016-17: Missed Opportunity to Address Inequality?

Oct 1, 2019 | oxfamadmin

Free The Night

Sep 9, 2019 | oxfamadmin

Woman, Open Your Eyes…

Oct 24, 2019 | oxfamadmin

From Darbhanga to Davos: Access to Affordable Medicine Still Remains a Key Question

Dec 16, 2019 | oxfamadmin

Hoping for a Second Chance: Punita Devi

Sep 27, 2019 | oxfamadmin

Activating Youth in Lucknow to Promote Girls’ Education

Sep 27, 2019 | oxfamadmin

Change is Coming: Rani Bitti’s Story

Sep 10, 2019 | oxfamadmin

Rachna’s Fight for Justice

Oct 7, 2019 | oxfamadmin

3 Key Observations from #WEF2016 that Indian Businesses Must Take Note Of

Sep 27, 2019 | oxfamadmin

Here’s Why States Need to Provide Free Basic Medicines

Nov 18, 2019 | oxfamadmin

Update: Oxfam to Provide Shelter to 300 Households Hit by The Manipur Earthquake

Apr 5, 2019 | oxfamadmin

In El Salvador, a struggle to survive El Niño

Oct 24, 2019 | oxfamadmin

Bihar designs a 15-year roadmap to reduce risk of disaster

Feb 20, 2020 | ursila

Violence as an Effective Mode of “Indian” Communication

Apr 5, 2019 | oxfamadmin

Because it’s 2015!

Sep 27, 2019 | oxfamadmin

Let’s welcome a new dawn, minus domestic violence

Oct 24, 2019 | oxfamadmin

Data and Discrimination: Women’s Ownership of Assets in India

Oct 24, 2019 | oxfamadmin

“No Woman, No Cry!”

Sep 27, 2019 | oxfamadmin

Pushing, pulling and the power of people: new horizons for corporate responsibility?

Jan 9, 2020 | oxfamadmin

Creating shared value through inclusive business

Oct 7, 2019 | oxfamadmin

TATA consultancy services – empowering farmers with mobile technology

Sep 27, 2019 | oxfamadmin

What the CSR numbers don’t tell

Oct 1, 2019 | oxfamadmin

6 important things companies need to do to be inclusive

Nov 21, 2019 | oxfamadmin

Why businesses need to invest in creating a productive population for a sustainable future

Sep 10, 2019 | oxfamadmin

Jaipur rugs – weaving the lives of the poor into the global markets. an inclusive business model.

Oct 24, 2019 | oxfamadmin

The next 15 years: highlighting the role of the private sector in development

Oct 7, 2019 | oxfamadmin

Emphasizing a human rights-based approach to inclusiveness in business

Oct 30, 2019 | oxfamadmin

Privatising Forests: A Bad Idea

Oct 30, 2019 | oxfamadmin

Adoption of Agenda 2030: 17 SDGs for 15 years

Nov 15, 2019 | oxfamadmin

Five questions about the #GlobalGoals you were too embarrassed to ask

Oct 7, 2019 | oxfamadmin

Last mile smile

Oct 7, 2019 | oxfamadmin

Social responsibility of companies should not stop at 2%

Sep 27, 2019 | oxfamadmin

In ‘campaign mode’, states flout FRA rules

Sep 27, 2019 | oxfamadmin

“I will not leave my forest. I will keep my jungle”

Oct 1, 2019 | oxfamadmin

Healthcare for all in India: When, How, and Why RSBY?

Oct 24, 2019 | oxfamadmin

Where is the nutrition? Ask pregnant women in a village of Bihar

Jan 9, 2020 | oxfamadmin

Learning to read at schools, but where are the textbooks?

Oct 24, 2019 | oxfamadmin

Progressive tax norms must underlie financing of the Sustainable Development Goals

Sep 27, 2019 | oxfamadmin

Teachers needed! Government schools are falling behind due to lack of funds

Oct 24, 2019 | oxfamadmin

Protect and expand India’s public healthcare system: The inequality imperative

Dec 16, 2019 | oxfamadmin

“On My Second Day At School, A Kid Asked Me What Caste I Was”

Oct 7, 2019 | oxfamadmin

India’s missing girls: A tale of healthcare neglect faced by girls

Sep 9, 2019 | oxfamadmin

Should we only give attention to women’s health on International day of action?

Nov 18, 2019 | oxfamadmin

No respite for 72-year-old Sitaram, a month after #NepalEarthquake

Oct 7, 2019 | oxfamadmin

One month on, education of children still jolted by Nepal earthquake

Oct 24, 2019 | oxfamadmin

New worry for Nepal; landslides, floods may block relief work

Oct 7, 2019 | oxfamadmin

Monsoon preview in Kathmandu blows away shelters in relief camp

Oct 1, 2019 | oxfamadmin

Last mile distribution of relief supplies is biggest challenge in Nepal: Indian ambassador

Oct 7, 2019 | oxfamadmin

When Delhi’s Streets Buzzed with ‘Haq Banta Hai’

Oct 7, 2019 | oxfamadmin

Lack of water, toilets making things worse for women in Nepal

Oct 7, 2019 | oxfamadmin

Oxfam India gets government approval to respond to #NepalEarthquake in 28 hours

Apr 5, 2019 | oxfamadmin

Desperation creeping in, people in Nepal wait for aid

Oct 7, 2019 | oxfamadmin

#OxfaminNepal: “More than 60,000 litres of water has been provided till now”

Oct 7, 2019 | Avantika

Political (and some other) priorities in Nepal as of 28 April 2015

Oct 30, 2019 | oxfamadmin

#Nepal Earthquake: “The death toll has crossed 2000 and this is just the beginning”

Jan 9, 2020 | oxfamadmin

#NepalEarthquake: It is going to be a long road to recovery

Oct 24, 2019 | oxfamadmin

Money Matters!

Oct 24, 2019 | oxfamadmin

All for Education, Education for All

Oct 7, 2019 | oxfamadmin

When schools continue to exclude, can education reduce caste discrimination in India?

Feb 20, 2020 | oxfamadmin

Ensuring the right to education, forming bonds for life

Oct 1, 2019 | oxfamadmin

How can India send a spaceship to Mars but not educate its children?

Sep 30, 2019 | oxfamadmin

India wins in cricket, but losing out on education

Sep 30, 2019 | oxfamadmin

Oxfam's 'Even it up' report a must read lesson on Inequality

Oct 24, 2019 | oxfamadmin

It’s time to understand ‘womanhood is beyond maternity’

Oct 7, 2019 | oxfamadmin

The True Measure of Land's Value

Oct 7, 2019 | oxfamadmin

The “Ten-thousand Committee”: Reviving VHSNCs in Jharkhand

Oct 1, 2019 | oxfamadmin

Singing their way out of child marriage

Sep 10, 2019 | oxfamadmin

Land Acquisition bill tests government’s pro-poor stance

Oct 1, 2019 | oxfamadmin

Breaking the silence, standing tall

Sep 27, 2019 | oxfamadmin

Making a Song and Dance about Child Marriage

Oct 7, 2019 | oxfamadmin

Let’s Talk About Sex

Sep 10, 2019 | oxfamadmin

Mobile technology solutions could be a game changer for maternal health: Scribes

Sep 27, 2019 | oxfamadmin

Missing Girls: The Puzzling Domestic Violence Agenda

Oct 3, 2019 | oxfamadmin

Her Ghar: A right to residence for every woman

Oct 7, 2019 | oxfamadmin

Considering Gender: A Mediaperson’s Guide to Covering Disasters

Dec 16, 2019 | oxfamadmin

True Grit

Apr 5, 2019 | oxfamadmin

Violence against women and star power: Does their magic wand work?

Oct 24, 2019 | oxfamadmin

Having Those Difficult Conversations

Oct 24, 2019 | oxfamadmin

Day of the Man: guarding the china shop

Oct 7, 2019 | oxfamadmin

Gender parity needs to begin at home with mother’s guardianship rights!

Sep 9, 2019 | oxfamadmin

It’s a Girl!

Oct 1, 2019 | oxfamadmin

Let’s Help End Domestic Violence!

Oct 24, 2019 | oxfamadmin

A Few Good Men

Oct 7, 2019 | oxfamadmin

Promises to keep—Implementation of PWDV Act in Odisha

Sep 27, 2019 | oxfamadmin

Make 16 Days of Activism an Everyday Practice

Oct 30, 2019 | oxfamadmin

Witch-Hunting: A less talked about form of Violence Against Women

Oct 24, 2019 | oxfamadmin

Markets Also Discriminate

Oct 7, 2019 | oxfamadmin

Let’s Talk About Domestic Violence!

Oct 7, 2019 | oxfamadmin

Getting Serious about Ending Violence against Women and Girls

Oct 3, 2019 | oxfamadmin

Right to a Violence Free Life

Sep 10, 2019 | oxfamadmin

It’s all about the money

Sep 10, 2019 | oxfamadmin

‘It’s No Longer Funny': The Funding Wars That’ll Dictate Our Future

Oct 7, 2019 | oxfamadmin

Girl, Interrupted

Oct 1, 2019 | oxfamadmin

16 Pictures From Imagining Inequality That WiIl Tell You The Truth #evenitup

Oct 24, 2019 | oxfamadmin

These 8 Goals Were Set To Develop The World, But 14 Years Since, This Is Where We Stand

Dec 5, 2019 |

A Look At The Year 2029: What Kind Of Legacy Will We Leave Behind For Our Future Generations?

Nov 18, 2019 |

These 8 Goals Were Set To Develop The World, But 14 Years Since, This Is Where We Stand

Oct 24, 2019 | oxfamadmin

BRICS bank a necessary step, but needs more transparency

Sep 9, 2019 |

Short term memory and Long term needs!

Oct 7, 2019 |

A people’s budget has to go beyond...

Oct 24, 2019 |

National Shame, National Failure

Sep 27, 2019 | oxfamadmin

Oxfam India pledges its support to #BringBackOurGirls

Oct 1, 2019 | oxfamadmin

Closing the Gap on Gender: Is India up for the challenge?

Nov 15, 2019 | oxfamadmin

She tills, she sows, but she does not own

Oct 7, 2019 | oxfamadmin

Take a pause: what do the Uttrakhand floods tell us about India’s development model?

Sep 10, 2019 | oxfamadmin

Saving lives on sharp turning roads

Oct 1, 2019 | oxfamadmin

They do mind the gap

Oct 7, 2019 | oxfamadmin

Right to Education, still a long way to go.

Oct 1, 2019 | oxfamadmin

Can We Close the Gap on Women's Inequality in India?

Oct 30, 2019 | oxfamadmin

Breaking Old Barriers and Building New Alliances for Food Justice in India and Globally

Oct 24, 2019 | oxfamadmin

Related Blogs

Stories that inspire us

17 Jan, 2017

NA

Unpacking the Risks of Doing Business in India

The World Economic Forum recently published its annual Global Risks Report for 2017. This report is based on a global perception survey covering various age groups, countries and sectors ...

26 Oct, 2015

NA

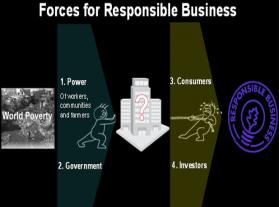

Pushing, pulling and the power of people: new horizons for corporate responsibility?

We all see that business shapes our lives. As consumers and workers, as farmers and communities, the behaviour of businesses has a deep impact on all of us. And we see that for a fair and...

26 Oct, 2015

NA

Creating shared value through inclusive business

The inclusive business concept aims to address poverty in a way that is commercially viable for businesses. It provides an opportunity to engage with poor people through interventions in ...

26 Oct, 2015

NA

TATA consultancy services – empowering farmers with mobile technology

Agriculture is a vital sector to the Indian economy, contributing to 23% of its GDP and employing half of the workforce. However, most rural Indian farmers remain poor and illiterate, wit...